Next Monthly Update: April 30, 2026

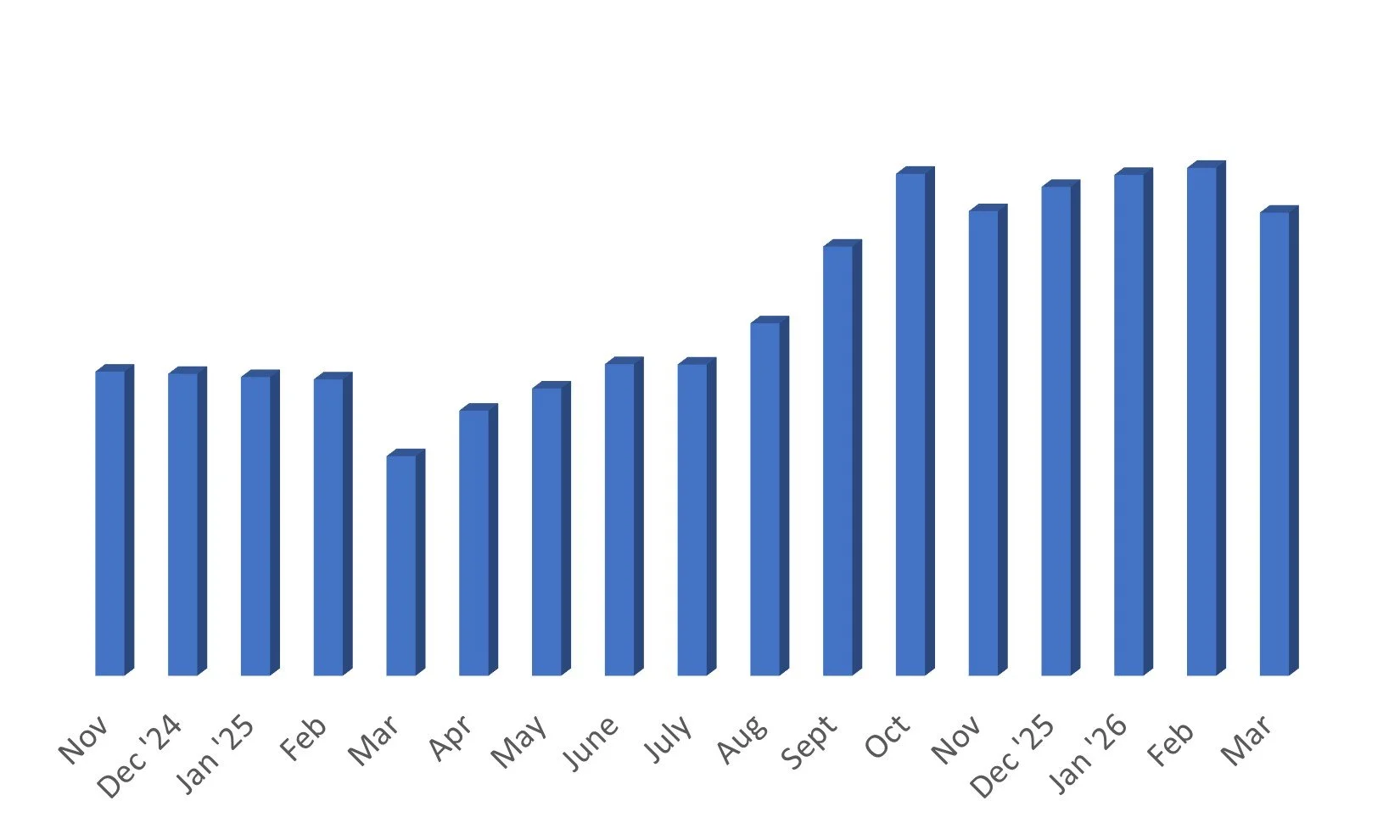

This Monthly Update: On March 31, 2026, my portfolio is down -5.26% YTD and up +48% after living expenses since inception. I have no credit card debt and am not keeping a separate rent cushion at this time. Just trimming and paying the rent. I’ll probably look to have a separate rent cushion around end of 2026. All taxes up to and including 2025 have been paid.

I have made no trades in about 6 weeks. The portfolio is down this year in March due primarily to the Iran war. I am expecting a very strong Q2 overall.

My goals are to consistently grow this figure on an annual basis, maintain zero or near-zero debt, improve the consistency of my investing/trading habits and execution, and take full advantage of compounding over time.

Next Weekly Update: April 24

This Weekly Update: April 17

Executed trades this week/summary: None. It’s been at least 8 weeks since executing a trade. The market has seen a v-shape recovery following the Iran War ceasefire.

News this week: GLSI announced they raised $10M through the ATM during Q1. Still very conservative dilution.

HROW announced that IOPIDINE 1% has been assigned a permanent j-code from CMS.

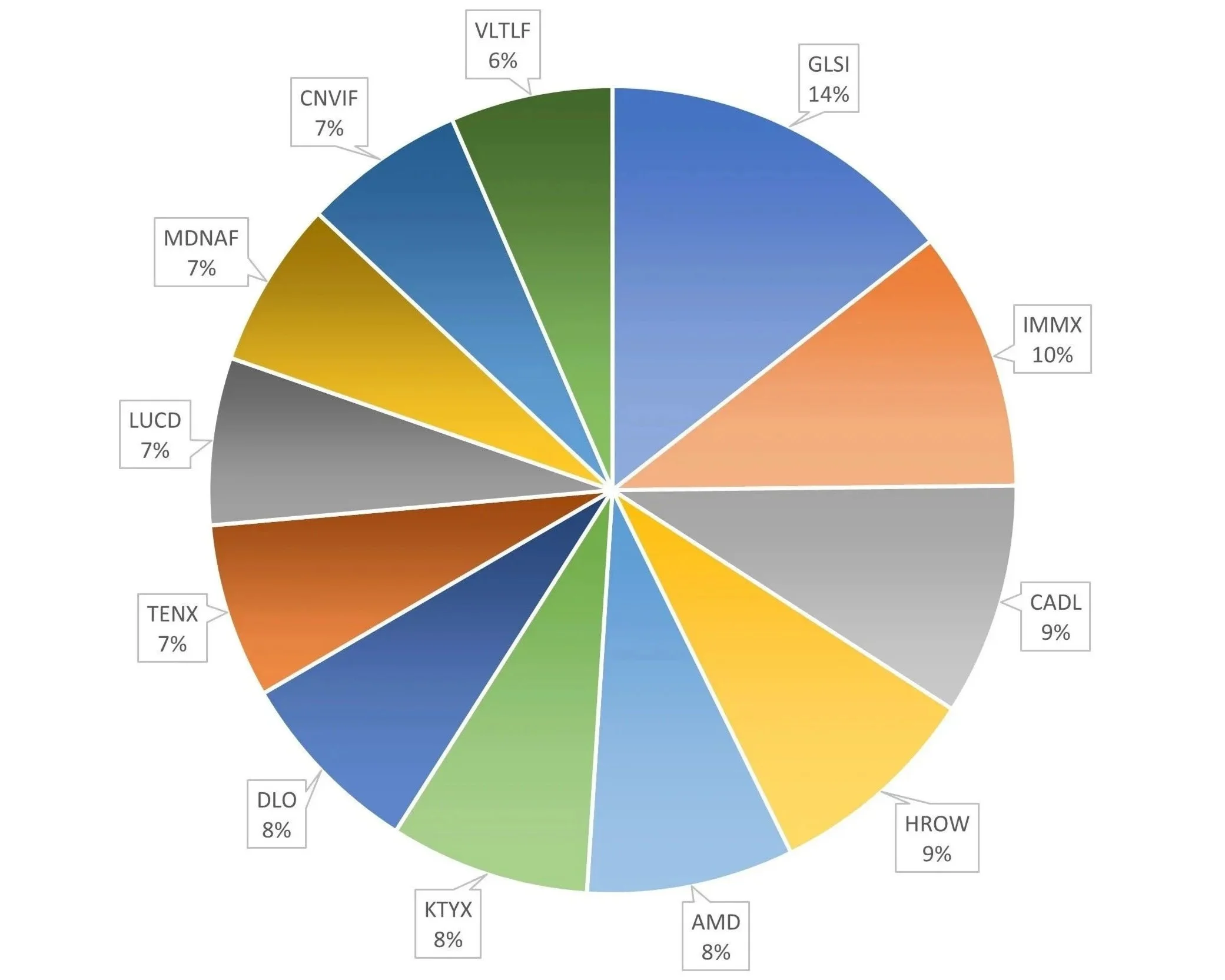

Number of holdings: 12

| Ticker | Company | Reason I'm Buying |

|---|---|---|

| DLO | DLocal Ltd. | Long-term holder and have traded DLO twice this year profitably. DLocal is the undisputed in cross border payments, particularly in emerging markets. They're growing and have a long runway. TPV is popping, revenue is growing rapidly, EPS continues to rise. The take rate is declining as expected and profit margins with it. While typical for this type of company, the market doesn't know yet how to value DLO given these dynamics. I think if the EPS continues to rise and FCF as well (though unlikely in sync short-term) over the long-term as I expect, this will continue to be very attractive. DLocal is one of the lowest risk investments in the market, in my opinion. Solid management executing flawlessly and consistently. Integrations and major partnerships are announced on a rolling basis.

|

| HROW | Harrow Inc. | Harrow is undervalued as an upcoming fastest growing ophthalmology company. They have the infrastructure, leadership, and execution to warrant a higher quarter over quarter growth rate than the market gives them credit for right now. A growth rate that should last for the next 6-8 quarters and beyond.

|

| VLTLF | LiberyStream Infrastructure | Previously Volt Lithium, LibertyStream is able to extract lithium from oil field brine, a waste product of oil drilling. This provides the opportunity for a second stream of income for oil companies and water treatment companies focused on extracting valuable resources from oilfield brine like LiberyStream's partner Wellspring Hydro. It also serves as a domestic supply of lithium for the US. The company has just recently completed the purchase of a small $2.5M chemistry set to convert their lithium chloride eluate to lithium carbonate, the finished product for the end user's requirements. We are waiting on JV announcement most likely with an oil company. The nearest competitor to VLTLF will require $1.5B and some years to construct their prototype whereas VLTLF is able to get going for just $20M and scale. JV announcement could be imminent.

|

| MDNAF | Medicenna Therapeutics Inc. | Long-term holder and have traded profitably once before. Medicenna is in Phase 1/2 for their engineered IL2 in multiple cancer types both as a monotherapy and in combination with Keytruda. Some background knowledge of the IL2 space is important to understand here. Pharma poured many $billions into IL2 because of the promise of stimulating the body's own natural immune response to fight cancer but toxicity levels were always too high. It has taken many years for the IL2 space to reemerge thanks to engineered versions, like MDNA11. MDNA11 selectively activates the "gas pedal" of the immune system (CD8+/NK cells) while removing the "brake" (Tregs) and the "danger" (Vascular Leak). It is still early but monotherapy results have been excellent and recent combination data with Keytruda - which would work with MDNA11 by then showing the immune system which cells are the cancer cells - shows promise. I believe this is an excellent candidate for large pharma to acquire. Recent deals and acquisitions in the space are in the $1-2B range and so far MDNA11 is proving it is the best in class. There are other drugs in the pipeline, but this is the one to watch. |

| CADL | Candel Therapeutics | It's been 20 years since there has been anything new for localized, non-metastatic prostate cancer. This drug has shown great efficacy and durability that could be best-in-class—partly because it is a class of one. We’re expecting one more data read on the full five years in Q2 to hopefully show continued durability. A BLA submission is planned for Q4 2026. Phase 2 in NSCLC showed excellent results last year; the company is focusing the Phase 3 (planned for initiation later this year) on non-squamous, given the stronger data compared to squamous in Phase 2. One more readout to show durability is coming in Q1 2026. With the recent raise at 5.45 and the $100M royalty agreement providing non-dilutive financing (assuming the drug is approved), the runway is clear for the foreseeable future. I expect the stock to double by Q1 2027. |

| TGTX | TG Therapeutics, Inc. | Leaving bc while I don't own at the moment, I often do. Second trade for me. First was profitable, around 30% gain. The stock has since fallen near where I'd previously bought it at 27+, now 30+/share. Briumvi is FDA approved for adults with relapsing forms of multiple sclerosis (MS), including clinically isolated syndrome (CIS), relapsing-remitting MS (RRMS), and active secondary progressive MS (SPMS). The relapse rate is something like once every 90 years. The sales growth has been steady and is expected to continue. Once patients are on Briumvi, they stay on so what is almost the equivalent of recurring revenue and profits here are massive in time. By 2030, likely looking at close to $2.5B annual sales. Current trials are for a modified dose regimen for easier administration in-clinic and a subcutaneous at-home administration trial, the latter of which is the most market expanding opportunity and data will be available on that sometime in 2027. The Company is profitable and there is little chance of further dilution. |

| TENX | Tenax Therapeutics Inc. | Tenax Therapeutics ($TENX) is a high-conviction biotech play focused on TNX-103 (oral levosimendan), a potential first-in-class treatment for Pulmonary Hypertension in Heart Failure with Preserved Ejection Fraction (PH-HFpEF). The investment thesis is built on a massive, zero-competition market of over 1.5 million patients and a significantly derisked Phase 3 "LEVEL" trial. A December 2025 statistical assessment confirmed the trial is over 90% powered to succeed without needing to increase the patient count, a rare and bullish signal for investors. With approximately $105 million in cash providing a runway into 2027, the company is well-capitalized to reach its critical clinical goals. Looking ahead, 2026 is the definitive "catalyst year" for the stock. Tenax expects to complete enrollment for the 230-patient LEVEL study in the first half of 2026, followed by the release of Phase 3 topline data in the second half of 2026. Simultaneously, the company is advancing its larger, global LEVEL-2 study, which initiated in late 2025 to build the robust safety database required for FDA and global regulatory filings. Positive topline data later this year would likely trigger a significant rerating of the stock, as $TENX remains the only company with a treatment currently in Phase 3 for this specific, underserved indication. |

| GLSI | Greenwich LifeSciences | Long-term holder. Greenwich is in registrational Phase 3 for preventing breast cancer recurrence. Huge success in previous trial. 14 "events" needed to trigger the first interim analysis. Estimates from different AI tools put this somewhere between second half 2026 and second half 2027. I don't want to miss it. This could be a 1,000% gainer from here on positive results. CEO share purchases are consistent and high. A lot of skin in the game. On 12/5/2025, the Company announced they have enrolled 1,000 patients in either of the two HLA groups and will continue enrollment. There are multiple reasons why they cited. The adaptive protocol amendment, guided by the Steering Committee and emerging data on GP2 efficacy across HLA types, allows ongoing enrollment to generate more events for multiple interim analyses, refine cohort sizes, and support broader labeling claims (e.g., all HER2+ patients) while leveraging high screening rates (~150/quarter). This enhances regulatory flexibility and commercial potential without altering the primary endpoint power. The does not increase the time to interim analysis for which 14 "events" is required. An event here is defined as invasive breast cancer recurrence. |

| IMMX | Immix Biopharma Inc. | Market Monopoly: $IMMX is on track to deliver the first FDA-approved CAR-T for relapsed/refractory AL Amyloidosis—a "blue ocean" market with no current approved therapies and a potential $3B+ opportunity. Best-in-Class Efficacy: Recent Phase 2 data (ASH 2025) showed a 75% Complete Response (CR) rate, which is projected to reach 95% based on current bone marrow markers. This dwarfs the <10% response rates of current salvage therapies. The "Outpatient" Advantage: Unlike existing CAR-Ts that require intensive hospital stays, $IMMX's lead asset (NXC-201) has shown zero neurotoxicity and ultra-short (1-day) side effects. This allows for outpatient administration, making it cheaper for insurers and more accessible to the 95% of hospitals that can't currently handle "toxic" cell therapies. Near-Term Catalyst: The company recently raised $100M to fund its 2026 BLA (Biologics License Application) submission. With a cash runway into 2027 and a clear regulatory path (RMAT designation), the 2026 approval is the primary value-unlock. Autoimmune Optionality: If the safety profile holds, NXC-201 is the perfect candidate to pivot into massive markets like Lupus or Myasthenia Gravis, where safety is the #1 barrier to entry. |

| KYTX | Kyverna Therapeutics, Inc. | KYTX is a "first-mover" play on the transition of CAR-T therapy from oncology into massive autoimmune markets, specifically targeting neuroimmunology. Pivotal Success in SPS: On December 15, 2025, Kyverna reported positive Phase 2 registrational data for its lead asset, miv-cel (KYV-101), in Stiff Person Syndrome (SPS). The trial met its primary endpoint with a 46% median improvement in mobility (timed 25-foot walk), significantly exceeding the 20% clinical benchmark. The "Safety Shield": Miv-cel is designed to be safer than oncology CAR-Ts. Across all indications (SPS, Myasthenia Gravis, Lupus), it has shown zero high-grade ICANS (neurotoxicity) and manageable CRS. This safety profile is essential for treating non-cancer patients who cannot tolerate high-toxicity profiles. Recent Funding & Runway: Following the SPS data, Kyverna closed a $100 million public offering (Dec 17, 2025). Combined with a $150 million debt facility secured in late 2025, the company has a cash runway into 2027, fully funding its operations through its next major regulatory hurdles. Imminent BLA Catalyst: Kyverna is on track to submit its first BLA in H1 2026 for SPS. If approved, it would likely be the first-ever FDA-approved CAR-T for an autoimmune disease, establishing a dominant market position. Broad Pipeline Upside: Success in SPS de-risks the platform for its other ongoing registrational trial in Myasthenia Gravis (Phase 3) and its expansion into Multiple Sclerosis and Lupus Nephritis. |

| CNVIF | Conavi Medical Corp. | First trade here for me. CNVIF is a "disruptive med-tech" play on the only imaging system capable of combining the two gold standards of coronary diagnostics into a single device. The "Hybrid" Monopoly: Conavi’s Novasight Hybrid System is the first and only platform to combine IVUS (ultrasound) and OCT (optical imaging) on a single catheter. This gives cardiologists a "super-view" of arteries that neither technology can provide alone. Imminent FDA Catalyst: In September 2025, the company submitted its next-generation system for FDA 510(k) clearance. A formal U.S. commercial launch is anticipated for H1 2026, which serves as the primary near-term price driver. Guideline Tailwinds: Global medical guidelines (ACC/AHA/ESC) recently upgraded intravascular imaging to a Class 1A recommendation (the highest level). This mandate is forcing hospitals to adopt new imaging tech, creating a massive organic growth wave for $CNVIF. Freshly Capitalized: Following a $20M institutional raise in 2025 and an ongoing January 2026 public offering, the company has significantly de-risked its balance sheet to fund the upcoming U.S. sales force and manufacturing scale-up. Rapid Revenue Growth: Revenue grew from $2.2M to $9.1M in the last fiscal year (+300%). Analysts project revenue to continue growing at over 50% annually as the U.S. launch commences. |

| LUCD | Lucid Diagnostics | The investment thesis for Lucid Diagnostics (LUCD) in 2026 centers on its transition from a clinical-stage diagnostic company to a commercially scalable oncology platform, primarily through its EsoGuard DNA test for the early detection of esophageal precancer. The bull case is anchored by recent major commercial wins, including a January 2026 U.S. Department of Veterans Affairs (VA) contract that grants access to nine million veterans, and a late-2025 unanimous expert consensus from the MolDx Contractor Advisory Committee supporting Medicare coverage. These catalysts address the company's historical "reimbursement gap," where high test volumes were previously unmatched by cash collections. With a strengthened balance sheet following a late-2025 public offering—extending the cash runway through late 2026—the thesis hinges on Lucid’s ability to convert its $35 million+ revenue backlog into realized cash and scale toward an estimated break-even point of 6,000 tests per quarter. While the stock remains a high-risk, micro-cap play with significant cash burn, the imminent finalization of a national Medicare Local Coverage Determination (LCD) represents a binary "inflection point" that could re-rate the company from a speculative venture to a high-growth medical technology leader. | AMD | Advanced Micro Devices | AMD is an AI chip company moving to full stack and competing directly with NVDA | NOW | ServiceNow | Leaving though I don't own at the moment, I may still buy back. Good opportunity. The Opportunity: The software sector has been hammered by "AI panic"—a narrative that autonomous AI agents will destroy seat-based licensing models. This fear has pushed NOW down nearly 30% YTD, hitting levels that decouple from its actual $600M+ AI contract momentum. The Catalyst: While retail investors are selling on "doomsday" headlines, C-suite conviction has shifted to a massive "buy" signal. CEO Bill McDermott and the executive team have taken the rare step of terminating their 10b5-1 trading plans (canceling pre-scheduled sales), with McDermott personally scheduling a $3M open-market purchase for late February. The Bottom Line: The "SaaSpocalypse" is an overcorrection. Insiders are actively betting that ServiceNow will be the "control tower" for AI agents, not its victim. With a $5B buyback authorized and the stock trading at a rare historical discount, the setup for a Q2/Q3 recovery is strong. |

On mobile devices the best view of the table below is likely horizontal orientation.